The Reserve Bank of New Zealand (RBNZ) has just trimmed the Official Cash Rate (OCR) from 3.25% to 3%, and the effects are already rippling through the property market.

Major banks including ANZ, Westpac, and Kiwibank have responded swiftly, cutting both fixed and floating mortgage rates. This change, while seemingly modest, signals a turning point for affordability and could be the catalyst that brings more buyers back into the market.

For Burberry Heights buyers, this is significant. A lower OCR not only reduces the cost of borrowing but also indicates a broader shift in the property cycle – one where demand is poised to strengthen, and prices could soon follow upward. The key question now is: how should you position yourself in this evolving market?

A Boost to Affordability

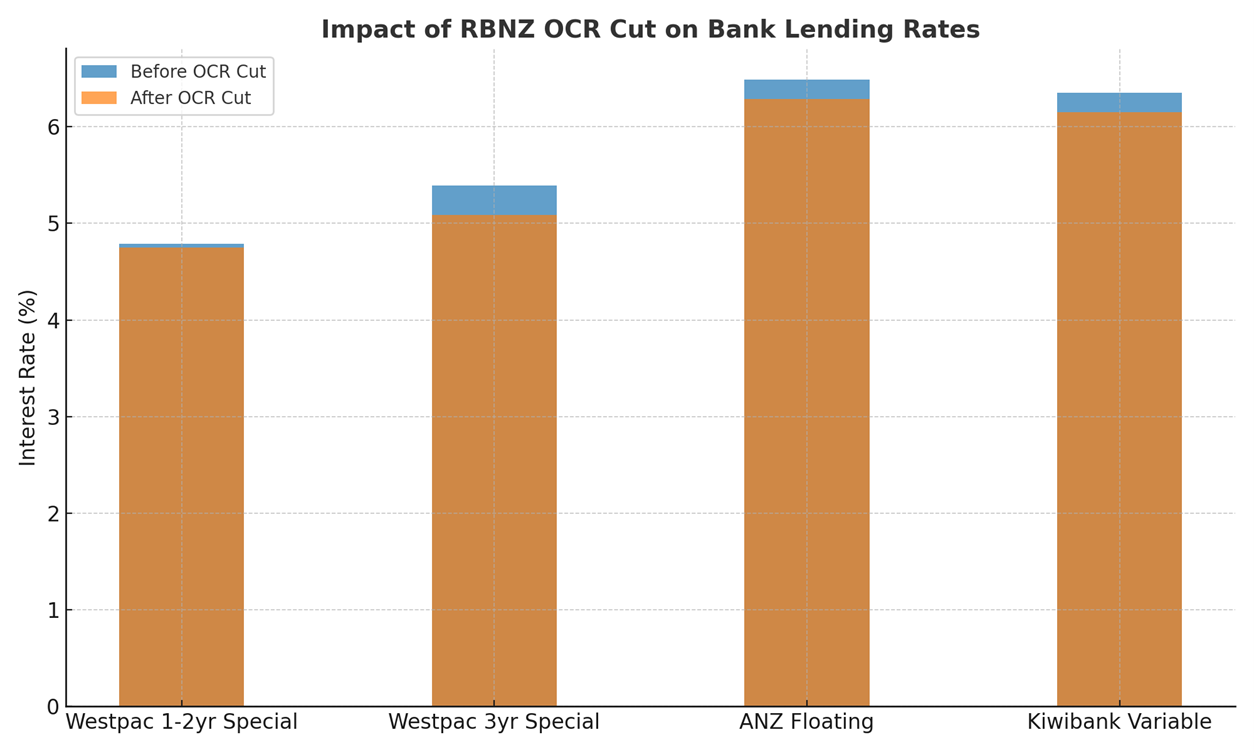

Westpac has set the tone by dropping its one-year, 18-month, and two-year fixed-term special rates to 4.75%, a new market low. Meanwhile, ANZ has trimmed its floating mortgage rate to 6.29%, and Kiwibank has reduced its variable home loan rate to 6.15%.

For context, just a few weeks ago, one-year mortgage rates across the major banks sat at 4.79%. While a drop of four basis points might not sound dramatic, when combined with other term reductions – such as Westpac’s 30bps cut on its three-year rate – the outcome is meaningful. On a standard $800,000 mortgage, even a 0.25% drop translates to savings of approximately $2,000 per year in interest payments. For households under pressure from rising living costs, this is a welcome reprieve.

Banks are also signalling greater flexibility with lending. By easing floating and revolving loan rates, institutions are making it easier for buyers to access credit. In practice, this means that buyers who were previously on the edge of borrowing capacity could now find themselves in a stronger position to secure finance.

Shifts in Market Dynamics

The OCR cut comes against the backdrop of a property market still finding its footing. According to the latest Onehub Market Report:

- Search activity is up 23% year-on-year, with 16.2 million property searches in July. This is a clear sign that buyers are paying attention again.

- The average expected sale value has eased to $998k, down 1% compared to the same month last year.

- Listings fell to 3,488 in July, but homes are taking longer to sell, with the average days on market sitting at 76.

This data paints a picture of a buyer’s market. Properties are available, buyers are engaged, but price expectations remain soft. Importantly, however, the gap between interest rates and affordability is narrowing. As lending costs fall and sentiment improves, the balance of power is beginning to shift.

Why Now Could Be the Sweet Spot

We are not yet at the stage where surging demand is pushing prices up sharply. But all the indicators suggest that moment is approaching. The OCR cut is widely seen as the first of several, with the Reserve Bank itself signalling that more rate reductions may be on the horizon. This mirrors moves across the Tasman, where the Reserve Bank of Australia recently cut its OCR to 3.6%, further reinforcing the regional trend toward monetary easing.

For buyers, this creates a window of opportunity:

- Affordability has improved, but prices have not yet rebounded.

- Banks are lending more readily, making finance approvals easier to secure.

- Market confidence is building, but competition is not yet at full strength.

It is often in these transitional moments that savvy buyers secure the best deals. As rates continue to drop, demand will inevitably lift. More buyers entering the market will gradually reduce the negotiating power of purchasers, shifting leverage back toward sellers.

Looking Ahead: Demand Will Drive Prices

A key driver of the next market phase will be the return of buyer confidence. With mortgage rates falling, the perceived affordability of homes improves. For example, at Burberry Heights, homes that may have felt out of reach just months ago could now be attainable within a typical buyer’s borrowing capacity.

At the same time, policy changes such as the anticipated relaxation of the overseas buyer ban for Active Investor Plus visa holders could introduce additional layers of demand. Migrants investing at least $5 million into the New Zealand economy are likely to target high-end property first, but the ripple effect will extend across the broader market. Increased competition at the top will free up demand across all tiers.

When combined with stronger domestic demand, this creates a powerful recipe for price growth. While the Onehub Property Price Index shows a slight dip now, the expectation is that values will begin to creep upward as these conditions materialise.

Affordability at Burberry Heights

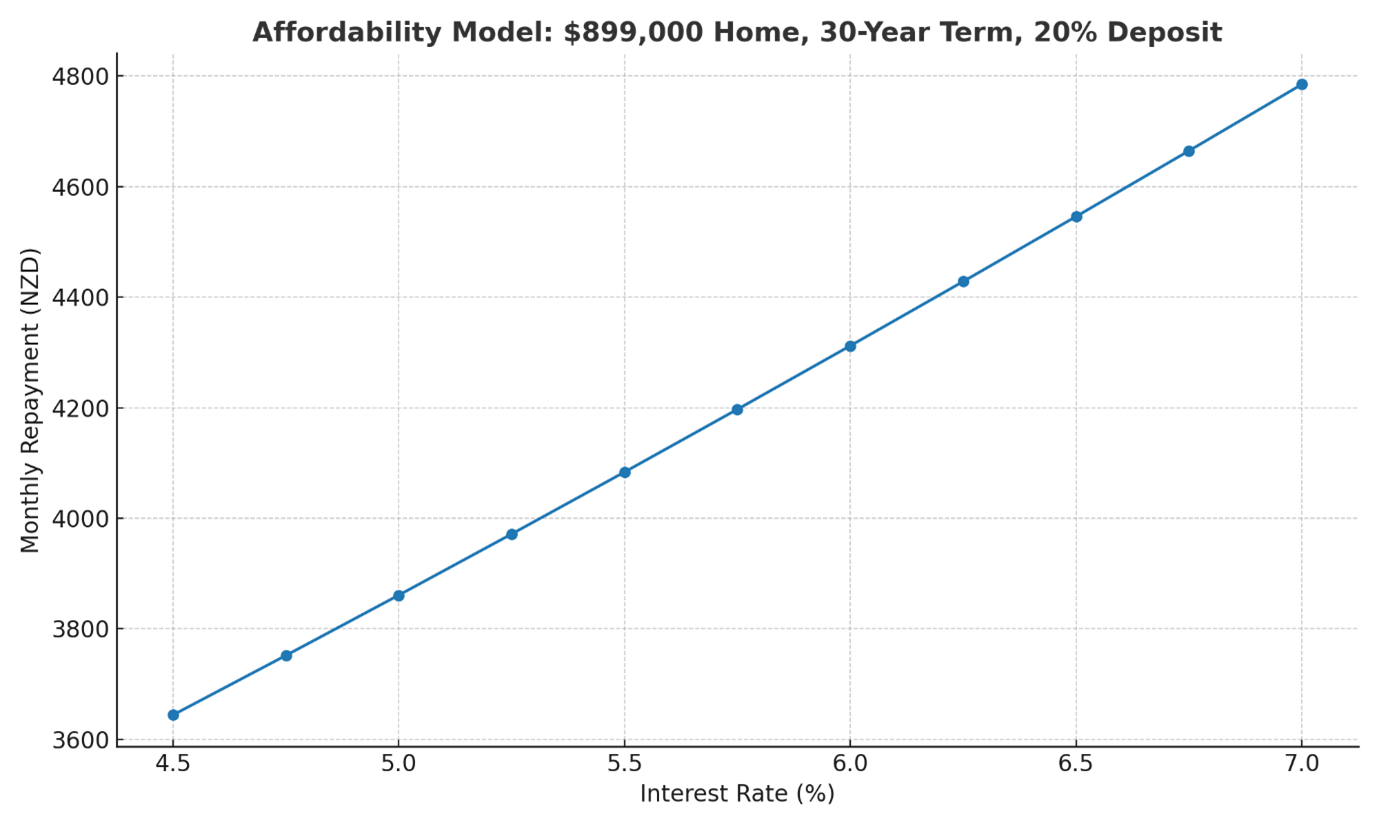

To illustrate how this plays out in real terms, consider a Burberry Heights home priced at $899,000. With a 20% deposit and a 30-year loan term, the difference between a 4.75% mortgage rate and a 6.75% rate is substantial.

At the current market-low rate of 4.75%, monthly repayments are around $3,762. At 6.75%, those repayments climb to over $4,645 – a difference of nearly $900 per month. This is why small changes in the OCR and mortgage rates have such a large impact on buyer behaviour.

Lower rates directly translate into more affordability, unlocking opportunities for more families to step into the market.

The Bottom Line

The market is at an inflection point. Interest rates are falling, lending conditions are easing, and demand indicators are turning positive. For Burberry Heights buyers, this means two things:

- Buying power has improved right now. Lower rates and a softer market make this a prime time to secure a property on favourable terms.

- Prices are unlikely to stay subdued for long. As more buyers re-enter the market, competition will intensify, and upward pressure on values will follow.

In short, today’s buyers are positioned to capture the best of both worlds – lower borrowing costs and still-accessible pricing. The opportunity is here, but it won’t last forever.

Thinking about making a move at Burberry Heights? Now is the perfect time while the market still leans in your favour.

Contact Nicolas Ching at 021 184 7777 or email nicolas@goodformliving.co.nz.

Alternatively, come see us in person at our open home at 99 Tributary Parade, Karaka

- Wednesday: 2:00 PM – 5:00 PM

- Saturday & Sunday: 11:00 AM – 4:00 PM