After several years of disruption, correction, and uncertainty, the New Zealand housing market is beginning to find its footing again. The excesses of the post-COVID boom have largely unwound, interest rates have stabilised, and buyers are re-engaging with greater confidence.

This is not a return to a speculative frenzy but it is a clear transition into a more constructuve phase of the cycle. For buyers and investors who understands how property markets move, these periods are often where long-term value is created.

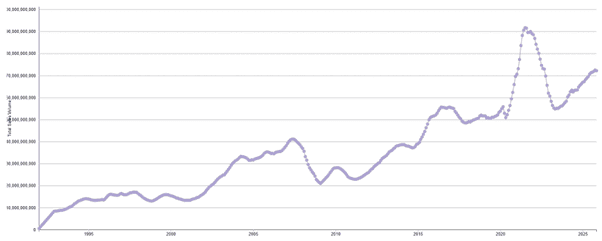

A Market Moving Out of Reset Mode

The past two years were defined by rapid interest-rate tightening, falling transaction volumes, and a sharp correction in prices. That adjustment phase now appears largely complete. National values remain meaningfully below their peak, but the pace of decline has stopped. In many regions, prices have flattened, and early signs of renewed demand are emerging.

This is consistent with a market that has moved through its downturn and is now stabilising. History shows that housing cycles rarely jump straight from correction to boom. Instead, they pass through a quieter recovery phase where confidence rebuilds, activity improves, and pricing firms gradually rather than explosively.

Source: REINZ

That is where New Zealand now sits.

Interest Rates: The Tailwind Has Run its Course, but Conditions Remain Supporting

Mortgage rates have fallen materially from their highs, easing borrowing pressure for households and improving serviceability across the board. While further meaningful declines now look unlikely, rates appear to be at or very close to the bottom of the cycle.

This matters because housing markets tend to respond not to falling rates indefinitely, but to certainty. Borrowers are increasingly accepting that current rates represent “the new normal” for the next phase of the cycle. As a result, deferred purchasing decisions are starting to move back onto the table.

Importantly, even if interest rates drift slightly higher in coming years, they are doing so from a position that is far more manageable than the peak settings of the past cycle.

From an affordability perspective, the sharpest adjustment is already behind us.

Price Outlook: Modest Growth, Not Mania

Most major bank and institutional forecasts are now aligned around moderate house price growth over the next year. Expectations generally sit in the mid-single-digit range, with annual gains of up to 6% widely anticipated.

This is not a speculative call – it reflects improving demand, stabilising credit conditions, and a gradual absorption of excess listings rather than runaway price inflation. In practical terms, it signals a return to normal market behaviour rather than exuberance.

Crucially, prices are still well below their previous highs. Buyers entering the market now are doing so at valuations that already reflect the correction, rather than pricing in optimistic future assumptions.

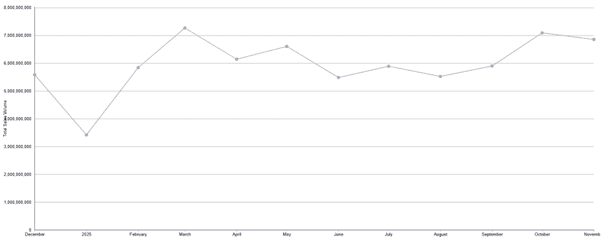

Stock Levels: Opportunity Still Exists – For Now

One of the defining features of the current market is the availability of choice. Listings remain elevated compared with the tight conditions of the boom years, giving buyers time, leverage, and optionality.

However, that balance is beginning to shift. Sales volumes are slowly improving, and stock is being absorbed faster than it is being replenished in many areas. This is how price pressure typically re-emerges – not through sudden demand surges, but through steady inventory drawdown.

Source: REINZ

Once excess stock clears, competition returns. Buyers who act before that inflection point tend to secure better outcomes than those who wait for “confirmation” that prices have already moved.

Who is Buying Right Now?

First-home buyers remain highly active, supported by improved affordability, KiwiSaver access, and lower deposit thresholds. Their sustained presence provides a stable base of demand and helps underpin market recovery.

At the same time, investors are quietly returning particularly at the more affordable end of the market. Improved cashflow dynamics and stabilising prices are making the numbers workable again, especially for those with a long-term view.

What remains subdued is discretionary upgrading activity. Many existing homeowners are choosing to stay put, limiting fresh resale supply. Over time, this dynamic tends to tighten stock further.

The Political Overlay: Timing Still Matters

With an election cycle approaching, policy uncertainty is beginning to re-enter market conversations. Historically, elections often encourage a degree of “wait-and-see” behaviour, temporarily suppressing activity.

For strategic buyers, this can create opportunity. Markets often price in uncertainty early, well before outcomes are known. Once clarity returns, confidence and competition can follow quickly.

This is one reason why early-cycle buyers tend to benefit disproportionately.

The Bigger Picture: Why This Phase is Often Missed

Property markets reward patience and foresight, not emotion. The strongest buying opportunities rarely feel obvious in the moment. They emerge when sentiment is improving, but before headlines turn optimistic.

Today’s environment fits that profile:

- Prices are no longer falling, but have not yet risen meaningfully

- Interest rates are stable and predictable

- Stock is still available

- Forecasts point to growth, not contraction

For buyers focused on long-term fundamentals rather than short-term noise, this is often where the groundwork for future gains is laid.

Final Thoughts

Markets move in cycles, and the most successful participants act before momentum becomes consensus. Waiting for full confidence usually means paying for it in higher prices and reduced choice.

New Zealand’s property market is not overheated. It is recalibrated, stabilising, and gradually improving. For those prepared to move while conditions remain balanced, the coming year offers a window that may not stay open indefinitely.

As the saying goes: the early bird gets the worm – but only if it recognises the opportunity early enough.

Developments to Watch: Burberry Heights and Watermere Residence

Against this improving market backdrop, it is increasingly clear that not all locations or developments will perform equally. Areas with strong infrastructure pipelines, relative affordability, and genuine owner-occupier demand are likely to lead the next phase of the cycle.

Within Auckland’s southern growth corridor, Goodform Properties has positioned two developments that reflect different buyer needs while benefiting from the same underlying fundamentals: population growth, transport investment, and long-term liveability.

Burberry Heights: Established, Premium, and Largely Spoken For

Burberry Heights represents the more mature end of the opportunity spectrum. Designed primarily for owner-occupiers and multi-generational families, it offers completed, move-in-ready homes with strong emphasis on space, quality, and everyday liveability.

The fact that Burberry Heights is now almost completely sold out is telling. In a market that has been cautious, buyers have still gravitated toward well-located, well-designed homes that offer long-term certainty rather than speculation. That depth of demand provides a useful signal of what the southern corridor is already delivering today – not just what it promises in the future.

For purchasers focused on capital protection, family living, and long-term ownership, Burberry Heights reflects the type of housing that tends to perform consistently across cycles.

Watermere Residences: The Next Phase of Opportunity

Where Burberry Heights shows what the area has become, Watermere Residences points to what comes next.

Comprising 12 new duplex homes priced from $799,000, Watermere is deliberately positioned to remain accessible – appealing to first-home buyers, younger families, and investors seeking entry into a growth location before it is fully realised.

Groundworks are already underway, with completion targeted for Q4 2026. That timing closely aligns with major transport and infrastructure milestones across the wider southern corridor, meaning buyers are effectively stepping in ahead of the curve rather than chasing it.

In market terms, this is often where the best risk-adjusted opportunities sit: purchasing while choice still exists, pricing remains grounded, and future amenity is not yet fully reflected in values.

A Practical Example of the Broader Market Story

Together, Burberry Heights and Watermere Residences illustrate the broader theme shaping the New Zealand property market right now.

The recovery is not uniform, and it is not speculative. Instead, it is selective – rewarding locations with strong fundamentals and developments that match real buyer demand. As confidence continues to rebuild and excess stock is absorbed, projects like these provide a tangible example of how early-cycle opportunities can still exist within an improving market.

For buyers weighing timing decisions, the message is consistent with the wider outlook: conditions are no longer distressed, but they have not yet become competitive. For those prepared to act before the next phase fully unfolds, that balance can matter.

For more information, contact Nicolas Ching

📞 021 184 7777

✉️ nicolas@gfp.co.nz