The Reserve Bank of New Zealand has held the Official Cash Rate (OCR) at 2.25% in its first announcement of the year. On the surface, it’s a “no change” decision. In reality, it signals something more important for property buyers: stability.

After several years of rate increases, uncertainty, and cautious lending conditions, we are now in a holding pattern. Mortgage rates have largely stabilised. House prices remain flat. The panic has eased. The momentum hasn’t yet returned.

And that creates opportunity.

Where We’re Actually Sitting Right Now

Inflation is tracking back toward the Reserve Bank’s 1–3% target band. The labour market has cooled. Consumer spending remains cautious.

The Reserve Bank has made it clear it intends to keep monetary policy accommodative while the economy continues its recovery. At the same time, it has not signalled aggressive rate hikes in the near term.

For borrowers, this translates into:

- Short-term mortgage rates easing and stabilising

- No immediate pressure for sharp rate increases

- Banks competing again for quality borrowers

- House price growth forecast to be flat in 2026

Flat.

Not falling. Not rising. Flat.

And that’s significant.

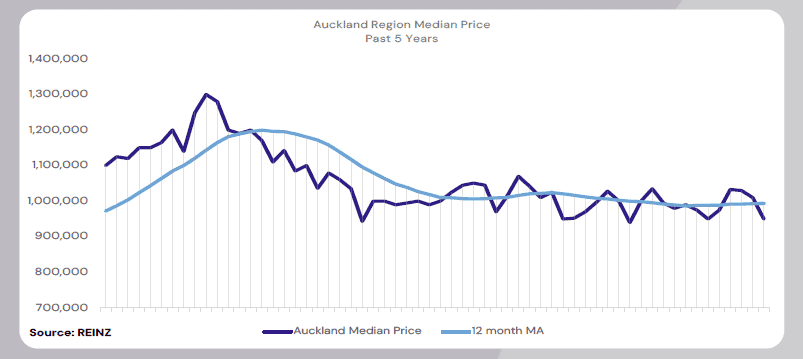

The Market Has Moved from Downtrend to Flat

Over the past 18–24 months, we’ve been climbing out of a downward cycle. Prices corrected. Buyers retreated. Confidence dipped.

Now we are sitting on the flat part of the curve.

Source: REINZ NZ Property January 2026

And historically, what happens after flat?

The next move is up.

Not overnight. Not dramatically. But momentum eventually returns once confidence improves and borrowing conditions remain steady.

The key difference is this:

When the market starts moving again, buyers move with it – and competition returns quickly.

If you wait until headlines say “property market rebounding,” you are already late.

You’ll be competing with more buyers.

You’ll be negotiating from a weaker position.

You may end up paying more than you would today.

The Power Dynamic is Favouring Buyers

Right now, many potential buyers are still sitting on their hands.

They are watching. Waiting. “Seeing what happens.”

That creates leverage for those prepared to act.

- Vendors are realistic.

- Developers are pragmatic.

- Stock is available.

- Negotiation power sits with the buyer.

When the market shifts upward, that leverage disappears quickly.

This is the window where disciplined buyers can secure value before broader confidence returns.

Mortgage Rates Have Stabalised

With the OCR steady at 2.25% and wholesale rates easing slightly, the urgency around locking in aggressively long-term rates has reduced.

While there is always global uncertainty, the immediate pressure that characterised the previous rate cycle has eased.

For buyers, this means:

- Greater predictability in servicing costs

- Less volatility in lending decisions

- A more balanced risk environment

When borrowing becomes predictable and prices are stable, the decision becomes strategic rather than reactive.

That’s a much stronger position to buy from.

What This Means for You

If you’ve been “hmm-ing and ahh-ing” about purchasing – waiting for clarity – this may be the clarity.

We are at the flat curve after a downward correction.

Mortgage rates are stable.

House prices are not rising.

Buyer competition remains moderate.

Those conditions rarely align for long.

The next phase of the cycle won’t announce itself politely. It will simply begin.

And once it does, buyers scramble.

New Builds: Lower Deposit, Stronger Position

Another factor many buyers overlook is the advantage of purchasing new build properties.

With qualifying lending criteria, first home buyers can purchase a new build with as little as 5% deposit.

For example:

A $799,000 four-bedroom property at Watermere Residences requires:

$39,950 deposit

This can come from savings, KiwiSaver, or a combination of both (subject to lending approval).

That lowers the barrier to entry significantly compared to traditional 20% deposits on existing properties.

Goodform Properties – Opportunities Available Now

Watermere Residences

Watermere Residences is a boutique collection of just 12 brand-new duplex homes, offering a curated mix of 3–5 bedroom layouts. Each home has been designed for practical family living, comfort, and functionality.

- Priced from $799,000

- Construction well underway

- Roof already in place

- Completion targeted for Q4 2026

A four-bedroom home at this price point, with a 5% deposit, places ownership within reach sooner than many expect.

Come see the development every Saturday and Sunday from 12pm – 2pm at 2 Wehi Drive, Karaka.

Burberry Heights

With only three premium duplex smart homes remaining, Burberry Heights combines intelligent design, integrated smart-home technology, and high-quality finishes throughout.

- Priced from $850,000

- Ready to move in now

These homes are complete. No waiting. No construction risk. Immediate lifestyle upgrade.

Join us at our Open Homes every Saturday and Sunday from 2pm – 4pm at 99 Tributary Parade, Karaka.

The Question Isn’t “Will the Market Recover?”

It’s “Where do you want to be when it does?”

Buying in a rising market feels safe – but it is rarely optimal.

Buying in a stable market, with negotiating power, predictable lending conditions, and subdued competition – that is strategic.

If this announcement has you reconsidering your timing, reach out to the Goodform team. We can walk you through deposit options, lending pathways, and what ownership could realistically look like for you.

Lending criteria applies, of course. But if you’re serious about exploring the opportunity while conditions favour buyers, now is the time to start the conversation.

For more information, contact Nicolas Ching

📞 021 184 7777

✉️ nicolas@gfp.co.nz

Join our WhatsApp Channel for the latest updates on all things NZ Property.